Securing business funding gets complicated when the rules are unclear and expectations are not in writing. For American small business owners, a loan agreement is your shield and guide, laying out every responsibility and deadline and minimizing costly disputes. With laws varying across the United States, using a customizable template helps you stay compliant and confident during the lending process, while protecting both your business and personal assets from legal surprises.

Table of Contents

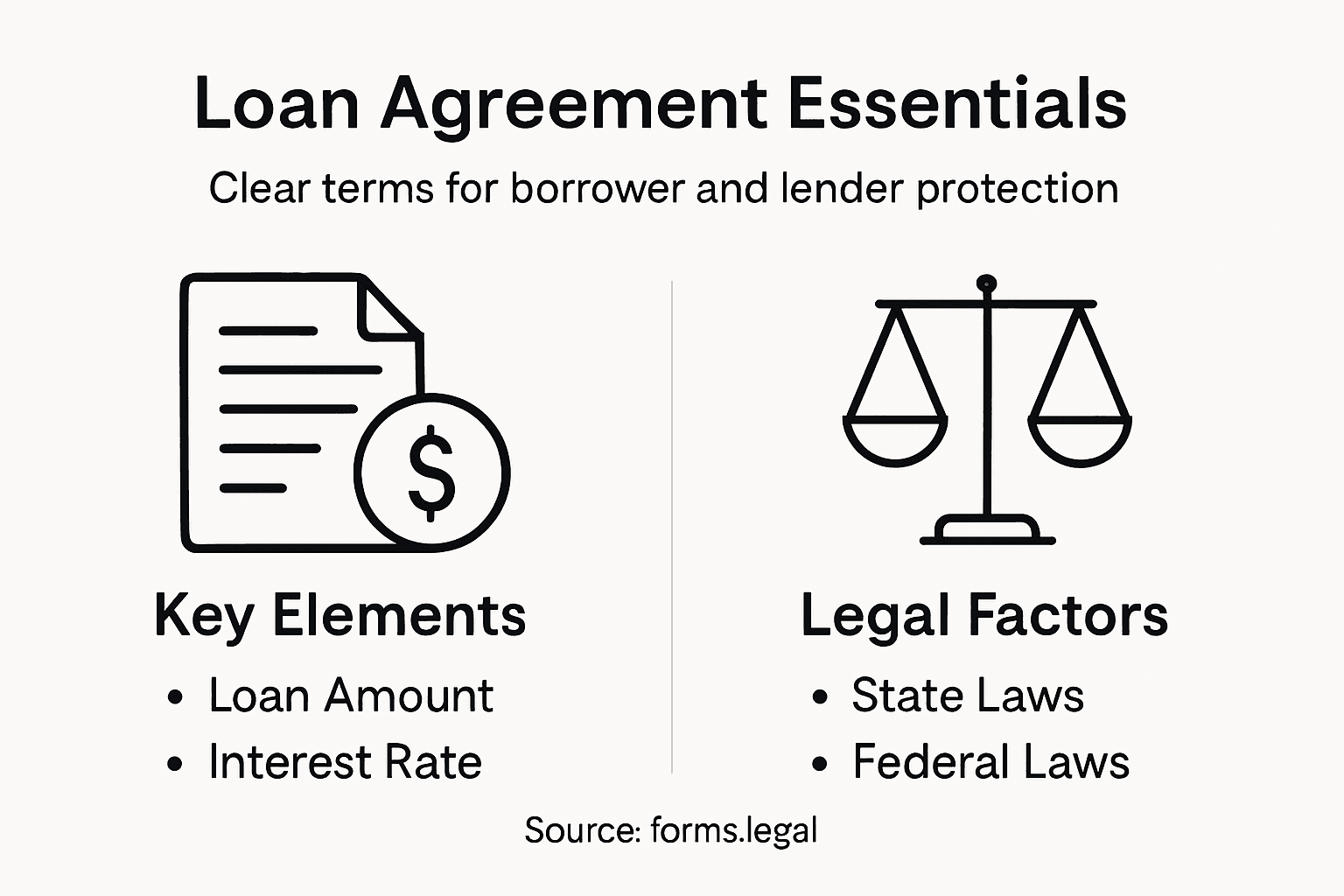

- Defining A Loan Agreement In Business Finance

- Types Of Loan Agreements For Small Businesses

- Key Provisions And How Loan Agreements Work

- Legal Requirements And Validity In The U.S.

- Borrower And Lender Risks And Obligations

Key Takeaways

| Point | Details |

|---|---|

| Loan agreements are essential | They clearly outline the terms of a loan, protecting both borrower and lender from misunderstandings and disputes. |

| Different types of loans serve various purposes | Choosing the right loan type for your business need helps in negotiating favorable terms and conditions. |

| Key provisions impact borrowers significantly | Understanding elements like interest rates, repayment schedules, and collateral requirements is crucial to avoid costly pitfalls. |

| Legal requirements ensure validity | Compliance with federal and state laws is necessary for enforceability, making it critical to utilize appropriate documentation. |

Defining a Loan Agreement in Business Finance

A loan agreement is a binding contract between a borrower and lender that outlines the exact terms of a loan. Think of it as the rulebook for your financing arrangement. It specifies who owes what, when payments are due, what happens if something goes wrong, and what happens if the borrower can’t pay back the money.

For small business owners, this document becomes your protection and your roadmap. The agreement defines each party’s responsibilities clearly, reducing confusion and disputes later. A loan agreement establishes the mutual promises that both the borrower and lender must keep, from the first dollar borrowed to the final payment made.

These agreements can take different shapes depending on your situation. A simple promissory note from a family member might be straightforward. A bank loan for your business expansion will be far more detailed. Regardless of complexity, every loan agreement should cover the loan amount, interest rate, repayment schedule, collateral (if any), and default terms.

What makes this document critical is its legal binding power. Once signed, both parties have enforceable obligations. The lender can pursue collection if you default. You have proof of your obligations and payment history. Without a written agreement, disputes become nearly impossible to resolve fairly.

State laws govern these agreements differently. Your Georgia business loan agreement works differently than one in Connecticut or Florida. That’s why using location-specific templates matters when you’re setting up proper documentation.

Pro tip: Download a state-specific loan agreement template that matches your location before meeting with lenders, so you understand standard terms and can negotiate confidently from the start.

Types of Loan Agreements for Small Businesses

Not all business loans look the same. Your needs determine which loan type makes sense, and understanding the differences helps you pick the right agreement. The major categories serve specific purposes and come with different terms, repayment structures, and qualifying requirements.

Term loans are straightforward. You borrow a set amount and repay it over a fixed period with consistent monthly payments. These work well when you need capital for equipment, renovations, or hiring. The lender knows exactly when they get paid back, so they often offer competitive rates.

Lines of credit function differently. Think of them like a business credit card with a higher limit. You access funds as needed and only pay interest on what you actually use. This works perfectly when your cash flow fluctuates seasonally or you need flexible working capital for unexpected expenses.

SBA loans deserve special attention for small business owners. The Small Business Administration backs these loans, which means lenders take on less risk and can offer better terms. The SBA 7(a) loan program includes multiple options tailored to different business needs, from standard term loans to specialized export financing. Qualification requires more documentation, but the lower rates and longer repayment periods often justify the effort.

Microloans serve businesses that can’t access traditional financing yet. These smaller loans (typically under $50,000) come from nonprofit lenders and community development organizations. They work well for startups or businesses rebuilding credit.

Here’s a side-by-side overview of common loan agreement types and their business uses:

| Loan Type | Typical Purpose | Repayment Approach | Special Consideration |

|---|---|---|---|

| Term Loan | Equipment, expansion | Fixed monthly payments | Competitive rates for assets |

| Line of Credit | Cash flow management | Pay interest on usage | Flexible access to funds |

| SBA Loan | Growth, refinancing | Longer repayment terms | Requires detailed documentation |

| Microloan | Startup or credit-building | Short loan duration | Smaller amounts, nonprofit lenders |

Each loan type has its own agreement structure. Understanding the differences between promissory notes and formal loan agreements helps you recognize what protections you have and what obligations you’re accepting.

Pro tip: Match your loan type to your specific need before shopping for lenders, so you can compare apples to apples and negotiate terms confidently.

Key Provisions and How Loan Agreements Work

A loan agreement isn’t just one page of terms. It’s a carefully structured document where each provision serves a specific purpose. Understanding what goes into these agreements helps you spot potential problems before signing.

The loan amount and interest rate are the foundation. The agreement states exactly how much you’re borrowing and what percentage you’ll pay as interest. Some loans have fixed rates that never change. Others have variable rates that adjust based on market conditions. Know which one you’re getting before you commit.

Repayment schedule tells you when money is due. This section specifies whether you pay monthly, quarterly, or in one lump sum at the end. It breaks down how much goes toward principal versus interest with each payment. Missing a payment date can trigger penalties or default clauses, so this timeline matters significantly.

Collateral provisions detail what assets secure the loan. If you default, the lender can seize these items to recover their money. A small equipment loan might use that equipment as collateral. A larger business expansion loan might require a lien on your business property or personal guarantee.

Covenants are rules you must follow while the loan is active. These might require you to maintain certain financial ratios, keep adequate insurance, or get approval before taking on additional debt. Covenants protect both the lender and borrower by establishing clear expectations and preventing actions that could jeopardize repayment.

Default clauses spell out what happens when you don’t hold up your end of the agreement. Late payments, missed payments, or breaking covenants can trigger acceleration (demanding full repayment immediately) or collection actions. This section is where your obligations become legally enforceable.

This table summarizes key loan agreement provisions and their impact on small business owners:

| Provision | Business Impact | Common Pitfalls |

|---|---|---|

| Interest Rate | Affects total loan cost | Not checking fixed vs variable |

| Repayment Schedule | Determines cash flow needs | Missing payment deadlines |

| Collateral Requirement | Puts assets at risk | Underestimating seizure risk |

| Covenant Clauses | Restricts business flexibility | Overlooking hidden obligations |

Pro tip: Before signing, highlight every deadline and covenant requirement in your agreement, then set calendar reminders 5 business days before each due date to avoid costly default situations.

Legal Requirements and Validity in the U.S.

Loan agreements must comply with federal and state laws to be valid and enforceable. This means more than just putting terms on paper. Lenders and borrowers both have legal obligations that protect their interests and ensure fair treatment.

Federal fair lending laws set the baseline for all loan agreements across the United States. The Equal Credit Opportunity Act (ECOA) and the Fair Housing Act prohibit discrimination based on race, sex, age, religion, national origin, and other protected characteristics. This means lenders cannot offer you different terms or refuse you credit based on these factors. Fair lending laws require transparent lending policies that treat all borrowers equally.

State laws add another layer of requirements. Each state regulates interest rates, disclosure requirements, and borrower protections differently. What’s legal in one state might violate regulations in another. That’s why loan agreements often include language specifying which state’s laws govern the contract.

Written vs. electronic agreements both carry equal weight legally. You might think a handwritten agreement or email exchange could substitute for a formal document, but that creates serious problems later. Electronic signatures on loan agreements are fully enforceable under federal law, meaning you can sign digitally with complete legal validity. However, the agreement must still contain all required disclosures and terms.

Disclosure requirements mandate that lenders provide specific information before you sign. Truth in Lending Act (TILA) requirements include the annual percentage rate, finance charges, payment schedule, and other key terms in a standardized format. These disclosures exist to prevent surprises and hidden costs.

Small business owners should know that personal guarantees create additional legal liability. When you personally guarantee a business loan, you become individually responsible if the business can’t pay. This extends the lender’s recourse beyond your company’s assets to your personal property.

Pro tip: Have a business attorney review any loan agreement before signing, especially if the document uses unfamiliar language or imposes personal guarantees that could expose your personal assets.

Borrower and Lender Risks and Obligations

Every loan agreement creates a balance of power and responsibility. Both borrowers and lenders take on specific risks and obligations that the agreement defines and enforces. Understanding what each side is responsible for helps you negotiate better terms and avoid nasty surprises.

Borrower obligations start with timely repayment. You must pay the exact amount on the exact due date, every time. Missing even one payment can damage your credit score and trigger penalty fees. Beyond payment, you’re responsible for maintaining any collateral in good condition. If you pledged equipment or property as security, you can’t sell it, neglect it, or let it deteriorate.

Financial covenants add another layer of borrower responsibility. These clauses might require you to maintain a certain debt-to-income ratio, keep a minimum cash balance, or avoid taking on additional large debts without lender approval. Breaking these covenants gives the lender grounds to declare you in default, even if you’ve made all your payments on time.

Lender obligations are more limited but still significant. Lenders must provide the funds they promised and follow all applicable laws. They cannot change terms arbitrarily or discriminate against you. Lenders also manage the loan responsibly, which includes proper record keeping and following regulatory requirements for loan servicing.

Collateral risk falls heavily on borrowers. Lenders require collateral to reduce their credit risk, especially for larger loans or riskier borrowers. If you default, the lender can seize and sell your collateral to recover what you owe. This means your personal or business assets are directly at risk if payments stop.

Default consequences extend beyond losing collateral. Borrowers who default face collection actions that can include wage garnishment, bank account levies, and severe credit damage. The lender can also pursue legal judgment against you personally, particularly if you signed a personal guarantee.

Pro tip: Before signing, create a detailed cash flow projection for the loan term to ensure you can comfortably meet payment obligations without risking default or covenant violations.

Secure Your Business with a Clear Loan Agreement Today

Understanding the importance of a well-crafted loan agreement is the first step to protecting your business and personal assets. The article highlights common challenges such as unclear repayment schedules, risky collateral provisions, and confusing covenant clauses. These issues can lead to costly defaults and unexpected financial stress. You need a solution that simplifies creating a legal, enforceable loan agreement tailored to your specific needs.

Take control now by accessing easy-to-use, attorney-crafted loan agreement templates on forms.legal. Whether you need a formal contract for a term loan, an SBA-supported arrangement, or a simple promissory note, our customizable documents cover key elements like interest rates, repayment plans, and default terms. Don’t risk misunderstandings or legal pitfalls. Start your loan agreement the right way with clear provisions and professional guidance at your fingertips. Visit forms.legal and draft your loan agreement today for peace of mind and strong legal protection.

Frequently Asked Questions

What is a loan agreement?

A loan agreement is a legally binding contract between a borrower and a lender that outlines the terms of a loan, including the loan amount, interest rate, repayment schedule, and what happens if the borrower defaults.

Why is a loan agreement important for small businesses?

A loan agreement protects both the borrower and lender by clearly defining their responsibilities, reducing the chances of disputes, and providing a roadmap for repayment, making it a critical document in business finance.

What are the common types of loan agreements for small businesses?

Common types include term loans, lines of credit, SBA loans, and microloans. Each type serves a different purpose and comes with its specific terms and repayment structures.

What key provisions should I look for in a loan agreement?

Key provisions to examine include the loan amount, interest rate, repayment schedule, collateral requirements, covenants, and default clauses, as these factors can significantly impact your financial obligations.